x= amount invested in A bonds

y= amount invested in B bonds

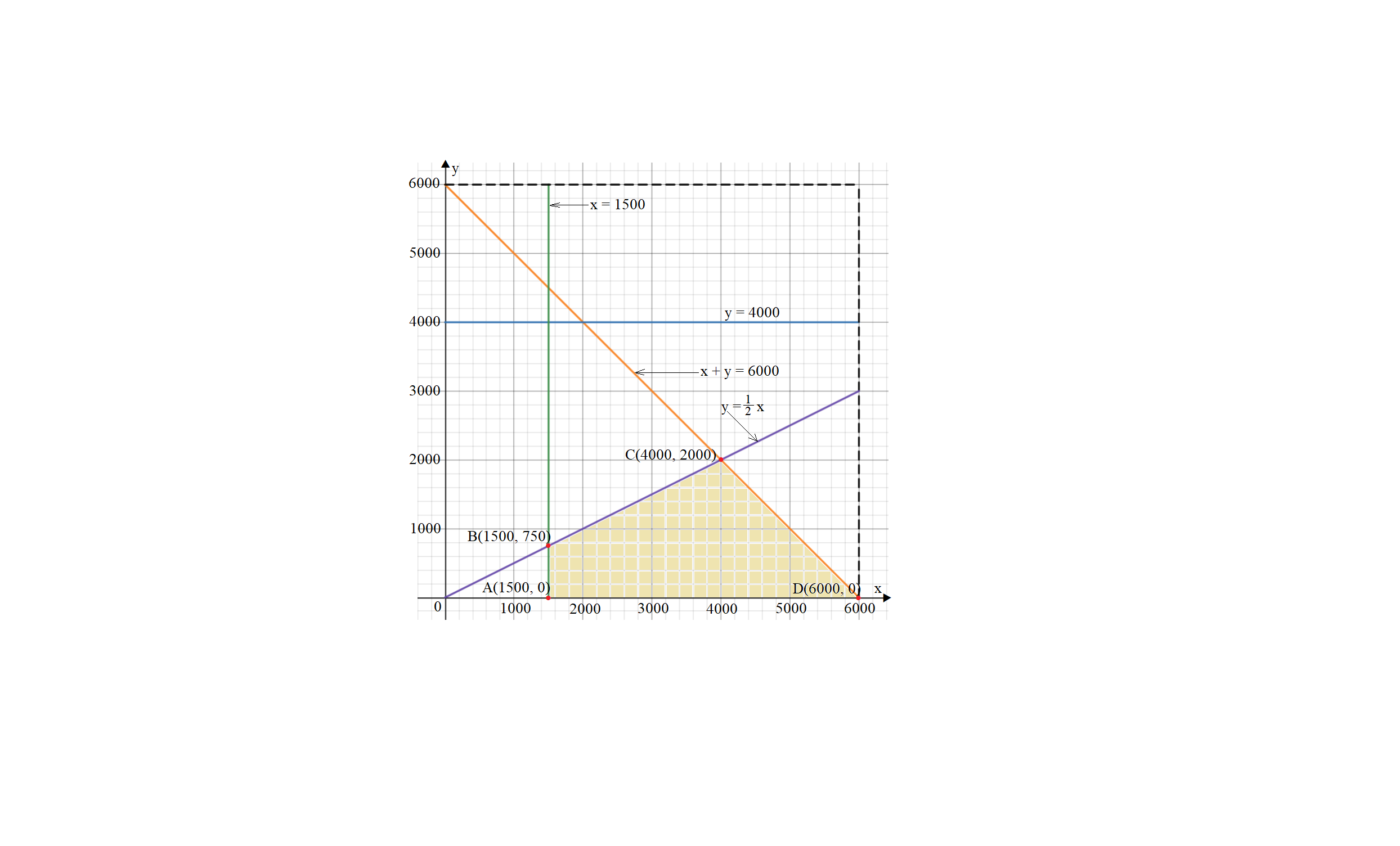

x+y≤6000

0≤y≤4000

x≥1500

y≤21xOur linear optimization problem is:

Maximize z=0.08x+0.1y subject to

x+y≤6000

0≤y≤4000

x≥1500

y≤21x

SegmentABBCCDDAEquationx=1500,0≤y≤750y=21x,1500≤x≤4000y=6000−x,4000≤x≤6000y=0,1500≤x≤6000z=0.08x+0.1yz=120+0.1yz=0.13xz=600−0.02xz=0.08x

PointA(1500,0)B(1500,750)C(4000,2000)D(6000,0)z=0.08x+0.1yz=120z=195z=520z=480

Because the point (4000,2000) produces the highest fund’s return we conclude that $4000 should be invested in

How much should be invested in bond A and $2000 should be invested in bond B.