To find the bond duration

The formula is given by

Duration =Y1+Y−C[(1+Y)T−1]+Y(1+Y)+T(C−Y)

where:

C= coupon rate

Y= Yield to maturity

T = Maturity

From the question, we have our parameters

C=12%, Y=10.8% and T=5 yrs

Converting from percentage to decimal

C=0.12, Y=0.108 and T=5yrs

Now, substituting the parameters into the equation

Duration =Y1+Y−C[(1+Y)T−1]+Y(1+Y)+T(C−Y)

=0.1081+0.108−0.12[(1+0.108)5−1]+0.108(1+0.108)+5(0.12−0.108)

=0.1081.108−0.12[(1.108)5−1]+0.1081.108+5(0.012)

=10.259−0.12[0.6699]+0.1081.108+0.06

=10.259−0.080+0.1081.168

=10.259−0.1881.168

=10.259−6.213=4.046

Hence, the Duration is 4.046

Now, to find the MODIFIED DURATION by the formula

modD =1+(nYTM)MacaulayDuration

Thus, we must firstly find the value for the Macaulay Duration.

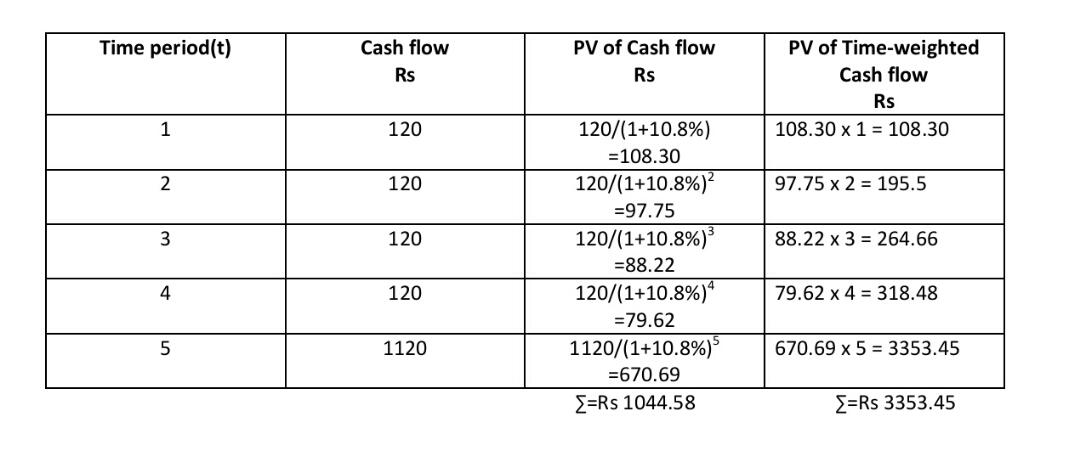

The tabulated data in the image below shows the Time period(t), Cash flow, PC of cash flow and the PC of Time-weighted Cash flow.

From the image, the summation of the PV of Time-weighted Cash flow is 4240.39 and that of the PV of cash flow is 1044.58

The Macaulay Duration for the 5 yrs bond is calculated as

MacDur =1044.584240.39

=4.06

Now, the Modified Duration given by the expression

modDur=1+(nYTM)MacaulayDuration

Where n=1 and YTM=10.8 %

modDur=1+(10.108)4.06

=1+0.1084.06

=1.1084.06=3.66

HENCE, the Modified Duration is 3.66